Since money spent on the wrong audience is wasted, it doesn’t make sense to target people with offers irrelevant to the consumer’s purchase journey. A college student is no more interested in a home equity line of credit than a homeowner is in a student account. If the content happens to reach potential customers at the right time, such as emails about low mortgage rates for someone searching for a home, prospects will be delighted rather than annoyed.

Thus, if local and regional banks focus on the digital capabilities and services most prized by their customers, they don’t need to check off every single digital box. There’s no point in investing in products that exceed the price point the target audience is willing to pay. For example, if market research indicates that most local customers would like peer-to-peer payments (P2P) and personal financial management tools, then an institution should invest in those features.

While virtual banking clearly muddles customer loyalty, most people remain anchored to their legacy institutions. According to J.D. Power’s 2019 U.S. Retail Banking Satisfaction Study, only 4% of consumers switched primary banks in 2018. The lack of switching doesn’t necessarily mean people are fully satisfied with their banks though.

To make sense of the changes in the financial sector, let’s start by identifying the reasons for digital banking’s appeal.

Mobile Lifestyles: In the Yes Marketing Survey, 42% of Gen Z respondents and 37% of millennials selected “ability to manage services via mobile app” among the top three factors they considered in a banking provider. In comparison, 34% of 38- to 52-year-olds selected this feature. Unsurprisingly, only 18% of 53- to 71-year-olds found a mobile app significant.

Millennials’ digital receptiveness makes sense considering they are the most mobile population, often traveling regionally or internationally for work and vacation. As the digital native generation, Gen Z is poised to adopt similar patterns in the workforce. With that in mind, out-of-network fees naturally grate on a traveler’s nerves. Also, the price of wire transfers is astounding when considering the convenience of P2P networks like Venmo and PayPal, which charge a minimal fee and send notifications of money transfers in minutes to people halfway around the world.

High-Yield Accounts: A 2% APY is quite attractive to someone who primarily uses savings and checking accounts. The lack of infrastructure and employees enable digital banks to offer high-yield accounts. These products are ideal for the mobile individual, or someone interested in earning decent interest from their deposit accounts. Add this perk to FDIC insurance, free ATMs, and low or no maintenance fees, and its no wonder younger generations flock towards digital banks. However, the lack of products compared to traditional banks, perhaps even checking accounts, might deter some from this option. That being said, the handicaps of digital banks will likely be resolved as processes become more sophisticated.

Bundling Services: In Cornerstone Advisors 2017 Q3 survey of 2,015 respondents, 40% of consumers who considered megabanks their primary institution would consider a bundled, fee-based checking account from Amazon. For a $5 to $10 monthly fee, the package would include services like cell phone damage protection and ID theft protection. In a culture accustomed to one-stop shops (i.e. Walmart and Amazon’s hold over retail), it’s understandable how open banking has reached such popularity. It’s simply convenient to aggregate the capabilities of multiple tools in one place.

Merchant Apps: While there is a push to centralize banking via mobile, payment methods are still segmented. Indeed, the Apple Card credit card developed in partnership with Goldman Sachs illustrates the marketing tactic of encouraging people to associate certain purchases with accounts. Examples include buying Apple products with the Apple Card to get cash back, and using the Starbucks Rewards Visa Card for Starbucks purchases. The Apple Card also offers financial management tools, such as a color-coded feature tracking a consumer’s card purchases by category. While Apple Card’s success is debatable, its collection of multiple features in addition to its primary function, a credit card, demonstrates the popularity of data aggregation.

Returning to J.D. Power’s 2018 Retail Banking Satisfaction Study, the report found digital-only customers, those who exclusively used online or mobile banking channels during the past three months, to be the least satisfied among banking customers (791 on a 1,000-point scale). In contrast, branch-exclusive customers indicated slightly higher rates of satisfaction, clocking in at 804. Lower satisfaction scores are attributable to three factors in the study: communication and advice, products and fees, and new account opening. When it comes to complex or costly transactions like stocks and mortgages, it’s not surprising people still want in-person advising.

The J.D. Power’s 2018 study also examined people’s willingness to switch banks, and openness skewed younger. Two out of five (40%) of 18- to 21-year-olds and 35% of 22- to 37-year-olds stated a willingness to switch. Older consumers might not only be skeptical of online banking, but also find it irrelevant to their needs. They might incentivized by loyalty programs more than younger generations as well.

The attachment that older populations have with legacy institutions starts early. According to a 2018 Bankrate and MONEY survey, the average U.S. adult has used the same primary checking account for 16 years. This narrative is common: someone opens an account for his child. From there, the child invests her first savings and checking account with the same bank. When it’s time for college, the teenager invests in a student account, unburdened by maintenance fees. By now, the college graduate has developed a deep enough trust with her bank to consult its advisors on mortgage loans. Once she starts a family, she opens a 529 plan for her own child, and the process repeats.

It’s undeniable that local and regional banks have an edge over large banks with customer loyalty. This advantage directly stems from community involvement. The widespread vision of a megabank as an impersonal entity, a suit that pushes one along through a loan process with no personal attention, won’t fade from the mainstream soon. Indeed, returning to the Cornerstone Advisors survey, only 15% of consumers who considered a community bank or credit union their primary financial institution would consider an Amazon bundled, fee-based checking account.

People feel connected to their communities when everyone at the local branch knows their name. This investment in local community is also partly why credit unions are often seen as preferable to banks. Credit unions are viewed favorably because of their nonprofit status, the ease of securing loans with them, and their lower interest rates. If people rooted in a community believe their financial provider serves a purpose beyond profits, they’ll be more inclined to pay a bit more for services.

It’s not just nostalgia and community that keep people using the same banks and credit unions, however.

In some cases, the inertia stems from people not knowing how good, or bad, a deal they are getting. It might be a hassle to switch from an account with a 1% APY to one with a 1.05% APY. Granted, people who earn virtually nothing on their deposit accounts might be astounded by such rates. Some checking accounts charge thousands of dollars to avoid monthly fees. Chase, for example, charges $12 a month if an individual does not maintain a daily balance of at least $1,500. Stiff maintenance fees make it particularly difficult for low-income individuals to maintain accounts in traditional banking systems.

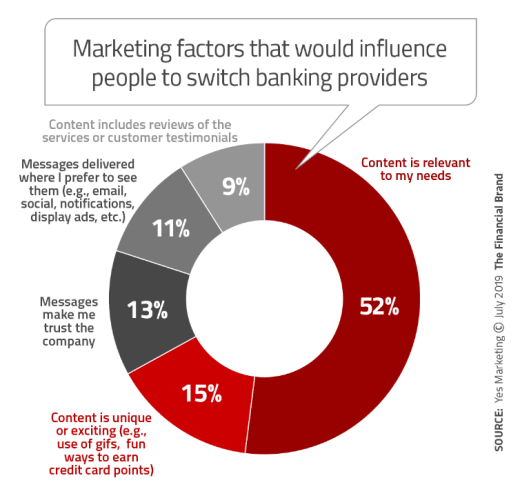

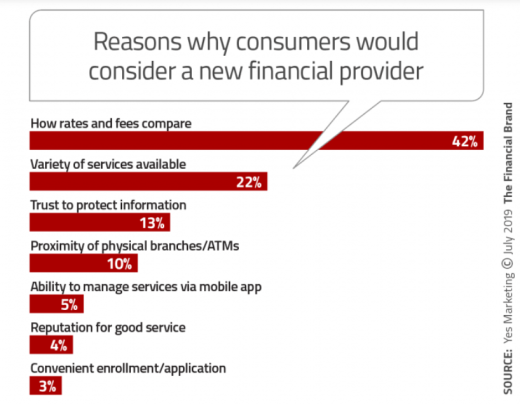

The fear of fees is an old pain point. Unsurprisingly, in a Yes Marketing survey, 42% of respondents selected “rates and fees” as their primary reason for considering a new financial provider. Resolving distrust isn’t as simple as it seems, however. People will be leery of hidden fees even if the sticker price is attractive. The Financial Brand pulled the following infographic from the Yes Marketing Survey: